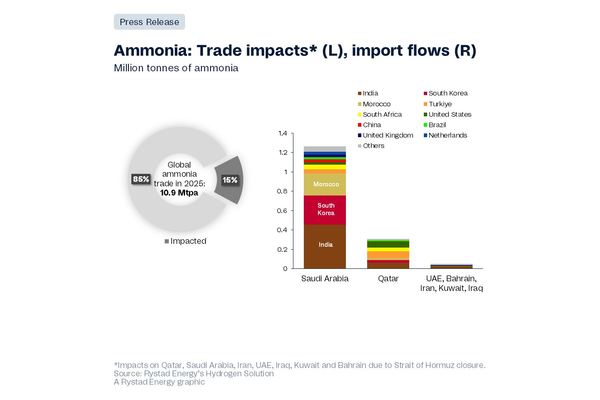

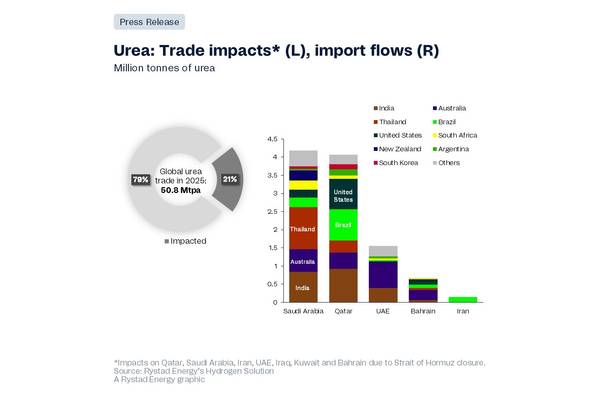

The trade of global fertilizer and ammonia faces intense pressure due to the effective closure of the Strait of Hormuz as diplomatic talks between the US and Iran remain uncertain. Rystad Energy’s 2025 trade mapping shows that the sale of 15% of global ammonia and 21% of urea, which is used as a high-nitrogen fertilizer, are tied to exporters potentially impacted by the closure. This includes leading producers Saudi Arabia and Qatar, followed by Kuwait, Bahrain, the UAE, Iran and Iraq. Our analysis predicts this sustained logistics shock will threaten the already strained ammonia and urea market and could quickly spill over to food and agriculture supply chains, starting with the countries most exposed to these trade flows.

“For policymakers and buyers, the energy security and food security message here is clear. More than one-fifth of urea traded by these Middle East exporters has direct implications for crop growth and farming, with India standing as the most exposed, importing around 6% to 8% of fertilizer from these Gulf countries. The strait’s closure can translate into real downstream risk quickly, including possible food shortages, manufacturing disruptions, compromised water integrity, and other significant global challenges, depending on the length of the war,” said Minh Khoi Le, senior vice president, and global head of hydrogen.

Other importing nations reliant on fertilizer traded via the strait are mainly located in Asia Pacific, including South Korea, Thailand, and Australia. Urea is also depended upon in the Americas, specifically the US and Brazil. Secondary markets that depend on re-exports from these countries will also be impacted. Key importers, particularly India and South Korea, would need to find other sources to feed their ammonia demands.

While producers with assets in other countries can ramp up fertilizer production, they are often in regions where the cost of production is much higher, such as in Europe, leading to higher food costs and potential inflation risks. However, recent green and electrolytic ammonia development can offer a possible solution, especially in the context of supply security, by detaching dependency of nitrogen fertilizers on fossil fuels. In a similar geopolitical climate, e-ammonia, or ammonia produced exclusively using renewable energy, was advocated as a solution to meet European energy demand after Russia’s invasion of Ukraine, yet with limited success. The alternative fuel is now being toyed with in China, however its success at replacing or displacing traditional fertilizer remains to be seen. Generally, e-ammonia costs are higher, but recent tenders from India have indicated prices close to parity with traditional ammonia. There are other offtake deals emerging across the market this year, for instance between Uniper and AM Green for e-ammonia generated in India and exported to Europe, or Yara’s offtake deals with ATOME in Uruguay. However, these volumes are expected to come online around 2030, so little relief can be expected in the near term.

The global ammonia trade stood at around 10.9 million tonnes per annum (Mtpa) in 2025, down from 12.3 Mtpa in 2024. Around 15% of this could be impacted by a prolonged closure of the Strait – mainly from Saudi Arabia, which would be impacted as most of the supply and trade is occurring on its east coast. Additionally, if there are disruptions to fertilizer supplies in agriculture sectors, Rystad predicts a decline in total global food crop production. For urea, the share of exposure is even greater. Global urea trade stood at around 50.8 Mtpa in 2025, of which approximately 10.6 Mtpa comes from the impacted countries – mainly Saudi Arabia, Qatar, and the UAE. Of this, 2.2 Mtpa was exported to India, again highlighting the nation’s dependency on fertilizer-related products from the Middle East. Other countries, such as Thailand, Australia, Brazil and the US, are all currently importing substantial amounts of urea from the region.

The event is not an isolated one for the fertilizer industry. Other trade corridors have already been under pressure in recent years. Russia’s volume has reduced significantly after its invasion of Ukraine, yet it remains a meaningful part of the fertilizer trade picture in 2025, at around 5% of global ammonia trade and 15% of urea exports. The recent events in the Middle East add another layer of risk to an already strained ammonia and fertilizer trading landscape, underscoring how concentrated these flows are through a small set of suppliers and chokepoints.