Compliance Costs Collide with Oversupply of Tonnage and a Challenged Economic Climate. Can operators cope? And, what will it cost them if they can? MarPro’s Barry Parker weighs in.

At a time when most maritime business sectors are suffering the pains of oversupply, the pace of regulation has also increased dramatically. In a business that went from the boom times of five years ago to near bust conditions for weaker players in 2012, penny pinching is now the norm. Nevertheless, the mandated costs brought on by regulation remain in the equation, whether we like it or not. And where choices are involved, how will shipowners analyze the alternative of a capital expenditure against cost savings in a future full of unknowns? A related question concerns the implications of regulation on the competitive landscape. For example, if everyone faces the same requirements, is one company (or segment) impacted disproportionately more or less than others? Any discussions of this type must also consider whether increased costs can be readily passed on to cargo providers in the form of increased freight rates or hires. So far, that – according to operators themselves – hasn’t been the case.

Much recent attention has been focused on mandated installation of equipment for ballast water treatment (BWT), where a clear implementation timetable has now emerged following changes to U.S. Coast Guard regulations earlier in the year. In late June, the new amendments – with the U.S. rules closely paralleling those of the IMO – took effect. Reduction of emissions resulting from fuel burned, along with overall energy efficiency, are topics that have been widely discussed. The coming of the North American SECA in August, and the IMO’s guidelines on the Energy Efficiency Design Index (EEDI- coming into force at the beginning of 2013), have brought these issues to the forefront. All of these variables have costs, sometimes dramatic, that have to be dealt with.

Investment in BWT, where there is a cost but not a financial “return on investment,” differs fundamentally from the choices facing consumers of fuels, where upfront costs (in a the form of a more efficient engine, a conversion to LNG fuelling, or purchase of a scrubber) are, in part, balanced against future cost savings.

Ballast Water Treatment

The market for retrofits of BWT systems has been estimated at around 40,000 vessels, according to Wartsila’s Tom Nyman, General Manager, Environmental Services, Water Solutions, who also points out, “There is concern over the supply of BWTs and with the installation skills and resources of the industry to handle so many retrofits.” Other estimates reach as high as 75,000 vessels to be retrofitted, where the preparation cost may rival that of the actual hardware.

An additional data point comes from Teekay Tankers, who operate a fleet that includes 28 owned vessels; some as old as 14 years and others delivered as recently as 2009. In its most recent “Form 20-F” (similar to an annual report), the company stated: “…we estimate that the installation of ballast water treatment systems on our tankers may cost between $2 million and $ 3 million per vessel.”

Teekay Tankers’ fleet of mainly Aframaxes and Suezmaxes would likely require BWT equipment with throughput capacities of at least 50,000 m3 and a relatively high pumping rate of 2,500 m3/hour, or more. Most deepsea newbuilds with keels laid after January 1, 2012 must include a BWT, with the cost included in the yard’s quoted price.

Costs of BWT extend beyond the capital expenditure. Data on annual operating costs is not widely available, and consultants’ estimates of such expenses have varied widely. An analysis by Lloyds Register published in 2010, reflecting input from multiple BWT suppliers, showed a mean estimated operating cost of $39 per 1,000 cubic meters (m3) of treated water. Depending on assumptions of system performance, system capacity and the number of yearly ballast voyages, this could equate to an annual operating cost in the region of $30,000 per vessel. Hence, in the case of our Teekay Tankers example, a $30,000 annual vessel cost could impact the bottom line by almost $1 million USD annually – not including off hire time (for installation) and unexpected maintenance issues.

SoX, NoX and Greenhouse Gases

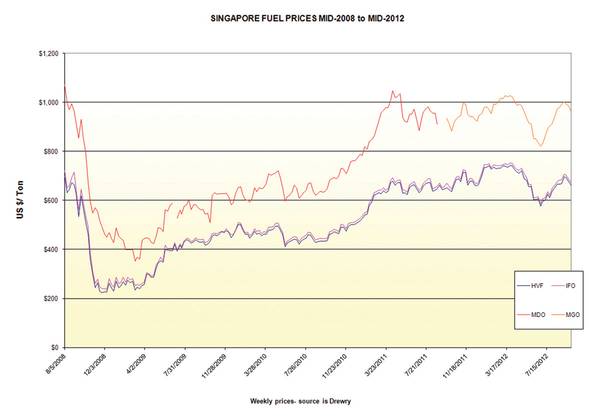

Reduced sulfur content in fuels has already cost shipowners plenty. The MARPOL Annex VI delineated timeline has already seen the worldwide sulfur cap drop to 3.5% (from 4.5%). In SECA areas – which now include North America – the cap will drop to 0.1% at the beginning of 2015 (from 1% presently). Worldwide, maximum allowable sulfur levels could drop to 0.5% as early as 2020 if the refining industry is able to provide sufficient low sulfur fuels. Peter Hinchliffe, Secretary General of the International Chamber of Shipping (ICS) said, in early October, “…the current 50% price differential between low sulfur distillate and the residual fuel oil that is currently in use is predicted to increase yet further if the new demand that will be created by the MARPOL requirements is not matched by increased supply.”

Owners face economic choices in meeting sulfur emissions requirements; however, the investment return is far from certain. Historically, differentials have varied widely, ranging from $200/ton to $500/ton; reduced distillate fuel supplies will lead to the higher distillate premiums alluded to by ICS Secretary Hinchcliffe. From a commercial perspective, owners must consider whether certain sectors or contractual arrangements might enable full or partial pass-through of increased fuel prices.

EEDI

Financial analysis is not straightforward. Analysts have suggested that the Energy Efficiency Design Index (EEDI), effective January 1, 2013, will bring about additional capital expenditures for newly ordered tonnage. Price data is sketchy, at best, for newly emerging alternatives, notably LNG fuelling. Ongoing political sparring on Greenhouse reduction further complicates matters; amidst an unclear set of rules, it is difficult, if not impossible to estimate costs (which could take the form of capital investment or fuel procurement choices) and benefits. In the latest twist, the European Union (impatient with the IMO’s perceived lack of progress and concerns about the efficacy of the EEDI) will begin monitoring maritime CO2 emissions in 2013. Financial executives, eager to gain visibility into future costs, are waiting to see whether the IMO adopts additional tools to reduce emissions, such as levies on fuel purchases, or development of a trading market for carbon credits.

The Germanischer Lloyd (GL) classification society, in conjunction with engine maker MAN Diesel, has conducted a rigorous economic analysis of investment in scrubber technology, in its early stages for vessels, and investment in ship’s engines burning LNG, where supply chains are only beginning to emerge.

Using scenarios of future pricing for heavy fuel, gas oil and LNG fuel, out to 2030, the researchers concluded: “Using LNG as ship fuel promises less emissions and, given the right circumstances, less fuel costs.” The lengthy analysis is heavily qualified, and is vessel and trade-specific; LNG’s advantage depends on a larger price difference for LNG versus heavy fuel, a reasonable cost for an LNG tank system and the percentage of operation within ECAs. Initial investments for scrubbers and for LNG systems, shown for a notional newbuild 2,500 TEU containership, are each around $5 million. The analysis also considers the installation of Waste Heat Recovery (WHR) systems, which adds approximately $4 million to the upfront outlay. For the basic LNG configuration, annual benefits, in the form of cost savings (compared to distillate fuels) are calculated to be around $4 million; when vessels spending a significant proportion of trading time inside ECAs, benefits rise and the theoretical “payback” times are calculated to be less than 12 months in the most optimistic cases.

Bottom Line – No Easy Answers

Because of the bespoke nature of cost economics, and the large number of variables involved, the next few years will be very busy for GL and others in the business of performing such calculations for shipowners. For the operators themselves, and given the likely ongoing constraints on sourcing capital, a wrong decision today could contribute to disaster tomorrow. The new cost of compliance comes at a particularly bad time. Yet, these costs are not going away and must remain a part of every owner’s financial planning.

(As published in the 4Q edition of Maritime Professional - www.marinelink.com)