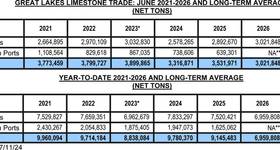

McQuilling Services Industry Note on 'Rebalancing Trade Flows: The New World Order' :

Many types of crude oil are produced around the world. Depending on the requirements of a particular refinery, a blend of heavy and light crudes is processed to manufacture a variety of petroleum products.

After peaking at 9.6 million b/d in 1970, US crude oil production steadily declined until reaching a low of 4.94 million b/d in 2008. From 1970 to 2008, US crude oil imports increased sharply to bridge the gap of decreasing domestic supply and increasing demand. In response to declining North American production and anticipation of rising heavy grade imports from the Caribbean, Latin America and Saudi Arabia, many US refineries were reconfigured to process a heavy crude slate in the 1990’s.

At the turn of the 21st century, rising global fuel costs led to advancements in crude oil extraction technologies, setting the stage for the development of the North American unconventional crude oil industry. Since 2008, supply from Canadian oil sands and US shale reserves have grown by 80%. The most significant aspect of the North American unconventional crude oil renaissance is the variety of crudes produced; the Canadian oil sands supply heavy crudes and US shale reserves supply light crudes. Because of the assortment of crudes available from unconventional plays, increased North American production has displaced a wide range of foreign crudes, which has led to a restructuring of long-established trade routes.

Canadian exports to the US have had a considerable impact on the global supply chain and we project that this phenomenon will escalate through 2019. Canada is a net exporter of crude oil and as productivity from their oil sands increases, Canadian exports to the US will expand as well. Due to intermodal transportation constraints, Canadian crudes are currently not reaching coastal ports to load tankers for more distant export markets in any significant volumes. The US is the main beneficiary of Canada’s growing export trade, absorbing approximately 97% of its international crude sales.

Since nearly all US shale production is light, heavy Canadian crudes are in high demand from US refiners. Gulf Coast refineries use a blend of light and heavy crudes to optimize the crude slate and increase operating efficiency. Considering the wide range of crude grades available from unconventional North American plays, commercializing the oil sands and shale industries has had widespread effects on global trade flows. Since 2005, exports of heavy Canadian crudes to the US increased by 1.5 million b/d, while the US simultaneously increased light crude production by 4 million b/d. The effect of rising North American heavy and light crude oil production on other trades is highlighted in Figure 1.

By 2014, US imports from Iraq, Mexico, Nigeria, Saudi Arabia and Venezuela declined by 2.7 million b/d from 2005 levels. Collectively, about 1.5 million b/d of heavy grade exports from Mexico, Saudi Arabia and Venezuela to the US were displaced by heavy grade Canadian crudes while the light grade Nigerian trade to the US was almost completely decimated by US tight oil production. As North American imports declined, the tonnage was absorbed into alternative markets. Figure 2 illustrates the trade flow shift that has taken place over the past decade.

In response to abating US imports, Nigerian exports have primarily been diverted to the Indian sub-continent and Europe. India’s economy is expected to grow by approximately 6.5% year-over-year through 2019. By 2019, India’s crude demand is forecast to grow by 40% over 2010 levels. Indian crude production is only foreseen to increase by 12% during the same period, suggesting a supply deficit that will drive greater crude imports.

Saudi Arabian exports to the US have declined by roughly 20% since 2005. The first significant decline in Saudi Arabian exports to the US, besides the 2008/2009 recession linked drop, took place in 2013 as a result of Canadian oil sands production growth. By 2014, Saudi Arabian exports to the US decreased by 20% over 2005 levels.

Growing demand from India and China has soaked up the lion’s share of displaced Saudi cargoes.As Canadian oil sands production expands in coming years, Saudi Arabian heavy grade crudes will continue to shift out of North American markets and into alternative growing markets, like China and India. By 2019, we expect that an additional 500,000 b/d of Saudi Arabian exports to the US will be displaced by Canadian oil sands production. It is our view that economic growth in China and India will generate enough demand to take in the displaced Saudi production, leading to increasing tanker demand on the AG / East trades. Trade flow rebalancing will be a central theme in tanker markets for the next five years. To better understand the changes in global trade flows and the impact on tankers, McQuilling Services has created a proprietary vessel deployment model. This model may help ship owners optimize fleet deployments by providing the most profitable triangulated trade routes across eight vessel classes. McQuilling Services will debut the vessel deployment model in the upcoming 2015-2019 Tanker Market Outlook, which will be released in January, 2015.