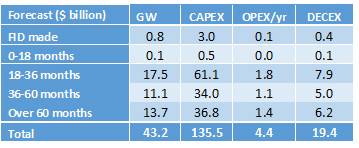

As of the end of January 2022, there were over 45 projects in development representing a $136 billion capital expenditure and $4.4 billion annual OPEX opportunity that are forecast to be brought on stream within this and early in the next decade.

What a difference a year makes. This time last year there was still some uncertainty around the federal offshore wind permitting process, the timing of offshore wind projects and certainty for the supply chain.

At the beginning of 2022 the situation is more positive. The final investment decision has been made for a major offshore wind project which has also reached financial close, 12 OCS projects are under final federal permitting review, 17.5 GW of project capacity has secured offtake commitments, 16.5 GW of new federal offshore leasing activity in the northeast, South Atlantic and California is underway, turbine component, foundation, and cable factories are being built in the U.S., awards for at least six Jones Act compliant wind farm support vessels were announced in the last quarter of 2021 and offshore wind port development is accelerating.

Our forecast and report accounts for 55 projects, 46 of which will install 43 GW of capacity in this and the next decade – and will require CAPEX amounting to $136 billion to bring onstream, a recurring annual OPEX of $4.9 billion once delivered, and $19 billion of decommissioning expenditure at the end of commercial operations

These are the findings shared in a recent report on the U.S. offshore wind market in this decade by Intelatus Global Partners (IGP).

The report examines the latest developments likely to drive offshore wind project development in the U.S. within this decade, forecasts the number, CAPEX, OPEX and timing of projects, and provides a roadmap to understanding and accessing these market opportunities.

Exhibit 1 CAPEX, Annual OPEX and DECEX Forecast by Final Investment Decision Timing

Source: Intelatus Global Partners

Source: Intelatus Global Partners

So, what has changed?

The excitement surrounding U.S. wind is founded on two power supply and demand drivers. On the supply side, federal leases containing over 20 GW of project capacity have been awarded – the last in early 2019. And more federal leasing is underway. On the demand side eight Northeast and Mid-Atlantic states have established offshore wind procurement targets and/or procured offshore wind capacity from developers operating federal offshore wind leases. Two Pacific coast states are also working through the process to establish offshore wind goals.

But those with a long memory of U.S. wind will remember the false dawn of the Cape Wind project. Initially proposed in 2001, Cape Wind secured the first commercial offshore renewable energy lease in the United States in 2010. The project’s construction and operations plan (COP) was approved initially by federal authorities in 2010 and revisions further approved in 2014. However, in the face of objections to the wind farm, Cape Wind relinquished the lease in 2017.

In 2021, three things changed and have created a more solid foundation for the U.S. offshore wind industry.

The first piece of the jigsaw was the White House initiative released in March 2021 to “catalyze offshore wind energy, strengthen the domestic supply chain, and create good-paying, union jobs”. The White House program included an offshore wind deployment target of 30 GW by 2030 and an aspiration to achieve 110 GW of offshore wind by 2050. The practical upshot is that developers and tier one suppliers, most with European wind industry backgrounds, have the visibility of demand needed to make domestic U.S. investments – including key component factories and port developments. This in turn will create employment opportunities for “tens of thousands of workers.”

Secondly, Federal agencies, led by the Bureau of Ocean Energy Management (BOEM), have shown a renewed impetus to progress offshore wind projects.

The 800 MW Vineyard Wind project was approved in July 2021 and reached financial close in September 2021. The project has broken ground, components are being manufactured, first power is expected in 2023 and the project will be fully commissioned in 2024. BOEM has approved the environmental impact assessment of a second wind farm, the 132 MW South Fork wind project and expects to complete final permitting of the project in January of this year.

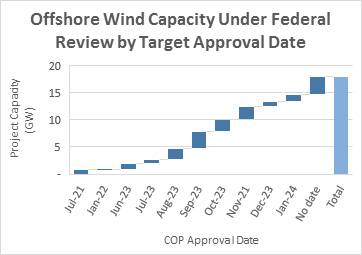

Exhibit 2 shows the clear pathway to project capacity permitting by the month and year when BOEM expects all permitting to be complete. Most project capacity will be fully commissioned three to four years after final permitting.

Exhibit 2 U.S. Offshore Wind Capacity by BOEM Permitting Target Date

Source: Intelatus Global Partners

Source: Intelatus Global Partners

The Department of the Interior has confirmed that BOEM will potentially hold up to seven new offshore lease sales by 2025. The first auction consists of six New York Bight leases. Other leasing will be held for sites in the North and South Atlantic, the Pacific and the Gulf of Mexico. This sets a clear foundation for long-term offshore wind activity in the U.S.

The third piece of the jigsaw is linked to state procurements and new federal leasing requirements– in simple terms developers must commit to significant supply chain infrastructure investment and make good on these commitments. As a result, developers are executing investments in offshore wind manufacturing and port infrastructure that were agreed as part of the capacity awards with the states. Further, the current New York Bight federal leasing contains domestic supply chain development incentives aligned to the supply chain development activities of New York and New Jersey. In its March 2021 statement, the White House targeted “one to two new U.S. factories for each major windfarm component including wind turbine nacelles, blades, towers, foundations, and subsea cables”. At the time this seemed somewhat optimistic, yet through state procurement requirements multiple key component factories are now being built and will provide ongoing opportunities to the domestic supply chain.

One piece of the jigsaw is missing – Jones Act Vessels

In the March 2021 White House statement on offshore wind, one ambition was to achieve “the construction of 4 to 6 specialized turbine installation vessels in U.S. shipyards, each representing an investment between $250 and $500 million.” Achievement of this goal is currently behind plan.

Till now only one Jones Act wind turbine installation vessel has been committed and is under construction – owned by Dominion Energy and under construction at Keppel Brownsville. Without additional domestic supply, developers will need to secure installation vessels from the international market – as Vineyard Wind has done for its project. However, although international supply of wind turbine installation vessels is growing, supply will be stretched in the global market around the middle of the decade – at the same time U.S. offshore wind installation activity is expected to peak.

Recently, Great Lakes Dredge & Docks announced that it is moving ahead with the construction of the first Jones Act compliant wind farm scour protection/rock installation vessel. The Ulstein designed vessel is being built at Philly Shipyards and is due to be delivered in late 2024. Great Lakes Dredge & Dock and Philly Shipyard have agreed an option for a second vessel to be declared at a later date.

One would expect there to be a significant amount of construction of service operations vessels (SOVs) and crew transfer vessels (CTVs). Both are used in the long-term operations and maintenance phase of a wind farm and will need to be Jones Act compliant. Till now one SOV has been announced as under construction – although the indications are that others are in the pipeline. In the CTV segment, three vessels, owned by Atlantic Wind Transfers and WindServe, are already operating on the Block Island wind farm and the Coastal Virginia Demonstration project. Five CTV awards have been announced recently awarded to two yards -- Blount Boats and Gladding Hearn shipbuilding. Despite the building activity, the domestic supply and SOVs and CTVs is significantly below our forecast for demand.

Floating Wind Advances

Many eyes are attracted to the potential of California’s offshore floating wind potential, with BOEM expected to auction two areas for development in 2022. But four floating wind projects are already currently being progressed in the Atlantic and Pacific -- three in state waters and two in Federal waters.

Floating wind requires a different supply chain approach to the bottom-fixed of the current northeast and Mid-Atlantic pipeline. First moves are being made on port infrastructure, but little movement has been made on the Jones Act vessels required to install floating wind projects – supply of the asset classes required in limited presenting a construction opportunity for domestic yards.

About the Author

Philip Lewis is Director Research at Intelatus Global Partners. He has extensive market analysis and strategic planning experience in the global energy, maritime and offshore oil and gas sectors. Intelatus Global Partners has been formed from the merger of International Maritime Associates and World Energy Reports.

For more information about the U.S. Offshore Wind Market Forecast, please visit www.intelatus.com or contact Michael Kozlowski at +1 561-733-2477or Philip Lewis at +44 203-966-2492