Outside investors and other variables change the way that shipping firms manage risk. Investable assets include ships, freight and even the hedging of bunkers.

"Shipping is now an investable asset,” was an important observation by analyst Tyler Rosenlicht, a research analyst at investment fund packager Cohen & Steers, speaking at the recent Capital Link conference on master limited partnerships (MLP) – a vehicle increasingly seen in shipping deal structures. Traditionally, shipping was a closed self-regulating game where everyone knew each other and therefore reputation mattered. One side of a deal would get comfortable (or not) with the ability of its counterparties to satisfactorily fulfill their commitments.

Outside Investors

The arrival of outside investors, an outgrowth of the strong markets for shipping assets from 2004 to early 2008 (just before the world’s financial crash), brought changes to the ways that risk was managed. Access to capital markets (to augment family money or to supplement bank debt) provided shipping companies with the wherewithal to ride the wave that was reminiscent of shipping’s glory days in the early 1970s. Such financings came with a price. New corporate cultures were required – professionalism and corporatization were now required, with disclosures to a new set of stakeholders – investors and regulators.

MLPs convey financial advantages, in the form of cheaper capital, for shipowners and for investors. They offer yields that compete with non investment grade bonds. The need for MLPs and partnership structures to lock in their cash flows for long periods provides part of the motivation of Dynagas LNG Partners LP (an owner listed on Nasdaq-GS with symbol “DLNG”), tied to the well know Prokopiou family, to enter into a 13 year time charter contract for its 2008 built 149,700 cu. m. vessel Clean Force (to be re-named Amur River) with Gazprom, the Russian gas marketer, commencing in July 2015 (following the expiry of its current charter, with BG Group Plc). The partnership’s three vessels will earn average hires of $78,200/day, once the new deal takes effect. Dynagas vessels are highly specialized assets. The company stresses that they are built for the specific purpose of moving LNG cargo (which may sometimes be exported from challenging environments such as, for example, the Yamal Peninsula in the north of Russia. Investors like the stability of cash flows that come from shipping partnerships and MLPs; at the end of April, GasLog (tied to the Livanos family) filed regulatory paperwork for GasLog Partners LP, which will own three LNG vessels on medium term charters to BG Group through 2018 and 2019, with charterers’ options to extend well out into the next decade.

The drybulk and tanker sectors see more risk, as charter terms are usually far shorter and the equipment is ‘commoditized,’ and vessel owners are ‘price-takers,’ not ‘price makers.’ In recent years, these markets have seen burgeoning markets in financial “swaps” that enable commercial risks to be better managed, on both the revenue and the cost sides. Tools for managing freight and fuel risks support the “investable asset” thesis, while also enabling owners, cargo interests, and operators of vessels to operate profitably. At a recent New York seminar organized by Clarksons Securities, an arm of the leading shipbroker, guest speaker Peter Sandler, from Edesia Asset Management said flatly, “Dry bulk freight is a commodity, not a service.” As such, Sandler characterized the present freight market as one of “low prices/high volatility,” explaining that the marketplace is subject to the vagaries of supply and demand, with high fixed costs, no way to store un-used capacity, and with very low barriers to entry.

In contrast to LNG vessels, where specialization and high capital cost converts into pricing power, drybulk owners are “price takers, not price makers,” in Sandler’s words. The Edesia fund, an offshoot of the Louis Dreyfus Investment Group, is an active participant in the freight derivatives market, which offers the ability to hedge risk, both short and long term, without committing to physical execution or engaging in counterparty risk.

Freight Derivatives

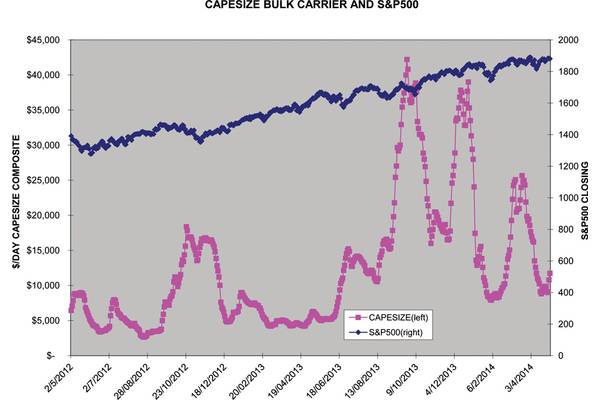

Clarksons’ team leader Alex Gray, described freight derivatives, usually handled over the telephone through brokers (just like shipping fixtures) as “The alternative to traditional period charters.” Sandler echoed this, saying: “Freight derivatives have changed the traditional method of freight risk management.” During a busy spurt, in late 2013, weekly trading in freight derivatives equated to 140 one year period timecharters – or, in other words, the traditional way of managing freight risk. If anything, drybulk freight is highly volatile. Data presented by Clarksons’ options expert Sander Bot showed the “annualized volatility” for the Baltic Capesize Index (a statistical measure of variations in a time series of shipping rates) was an off-the-charts 120% in the first two months of 2014.

In setting the stage for Sandler and the other speakers, Alex Gray enumerated some of the risk pitfalls in traditional charters, which include “the knock on effect of defaults through period relets, the failure to address and accurately assess counterparty risk, and too much reliance on tradition and trust.” The freight derivatives markets are able to overcome these issues because the vast majority are traded through a financial clearing-house, analogous to a central guarantor.

Speaker Isabella Kurek-Smith, representing LCH.Clearnet Group (with a majority ownership by the London Stock Exchange, and the balance by other exchanges, and the big brokerages) noted that 75% of drybulk cleared Forward Freight Agreements (FFA) are handled through her organization. In describing the evolution of the market, Kurek-Smith discussed consequences of the Dodd-Frank regulations aimed at the commodity swaps markets. Ship owners, charterers and freight traders may see changes in the way that their buy and sell orders are handled as financial swaps are re-categorized, for regulatory perspective, as futures contracts, but clearing- the central tenet of risk management and mitigation, will remain.

Fueling Anxiety: Hedging Risk in Bunkers

Ships’ engines require fuel, and the energy complex brings its own set of risk management challenges for shipowners. The fuel markets have also developed tools to enable fuel buyers to manage their price risk. A March, 2014 Connecticut Maritime Association presentation by Ebony Smith, from World Fuels Corporation (WFC), a supplier to maritime and aviation modes, showed annualized volatility of a “basket” of bunker fuels reaching nearly 35% during spurts in 2011, and exceeding 30% briefly in 2012. Passing on fuel price moves to charterers, a simple and effective way to manage risk may not always be possible, particularly in weak markets when the cargo interest has the upper hand. As Smith notes: “Ship operators are ‘short’ fuel and have inherent price risk.” WFC, based in Miami, and other large fuel suppliers, may serve as a dealer or risk management products to customers, or may, alternatively, manage the hedging, and embed the risk management features into a price.

As shipping companies court investors, risk management actually becomes a selling tool. One company listed in Norway, Western Bulk, uses the tagline, in its presentations, of: “Combining solid shipping experience with financial portfolio management principles.” Its presentations to the investment community discuss its unique business model, built on a “…decentralized and trading oriented business sophisticated risk control system…” with six full time employees monitoring freight and fuel risk using proprietary computer models. According to the company, “Models are run daily to measure and monitor exposure - useful as tools to understand value drivers and risk/return relationships…”

Managing Risk: the Bottom Line

A different variation on the portfolio approach, with implicit management of risk, can be found in Vancouver, at Teekay Corporation and its related companies. The corporate parent is on a path towards becoming an asset light holding company; separate subsidiaries (two of which are MLPs, where vessels are on long contracts) operate in the gas tanker, offshore oil, and conventional tanker segments. A newly launched arm, listed in the Norwegian market, will specialize in the admittedly risky strategy of buying attractively priced tankers and flipping them when the market goes up. The highly respected Teekay has therefore contained different risks in different silos – a simple yet seemingly powerful strategy.

Further dimensions of risk, sometimes learned the hard way, were enumerated by Jake Storey, who is Risk Manager at Gearbulk, an international drybulk shipping company based outside London, U.K. Storey, with a long history in the management and the owning sides, told Maritime Professional in May, “Whatever the market, it is imperative the effective counterparty risk is performed. Not just for legal compliance, but for commercial reasons as well. There are several companies that can support vessel owners and operators with counterparty risk assessment. However, in addition, the shipping industry group called the Maritime Anti-Corruption Network (MACN) supports companies in the maritime industry to address the corruption and compliance challenges that can arise with shipping,”

Good lessons indeed.

(As published in the 2Q 2014 edition of Maritime Professional - www.maritimeprofessional.com)