Dry bulk sector revisits 1980s lows and faces uncertain longer term outlook; with the market near bottom, attention is turning toward the length of the downturn, the effect on asset values and the impact of broader demand side changes.

In terms of annual average fleet employment rates, the dry bulk market has now dropped to levels last seen over 20 years ago in 1992, according to the latest quarterly dry bulk market forecast from Maritime Strategies International (MSI).

However, current time charter rates of $5,700/day for Panamax vessels are much worse now than the $9,500/day rates seen then. It is necessary to look back to 1986 to see nominal timecharter rates as low as today in annual average terms.

The spot market is in even worse condition: according to a theoretical voyage cost calculation across a representative sample, almost a fifth of aggregate earnings for Capesize vessels on the spot market would have been negative this year to date, taking into account individual vessel fuel consumption characteristics.

Asset Values at Scrap-plus

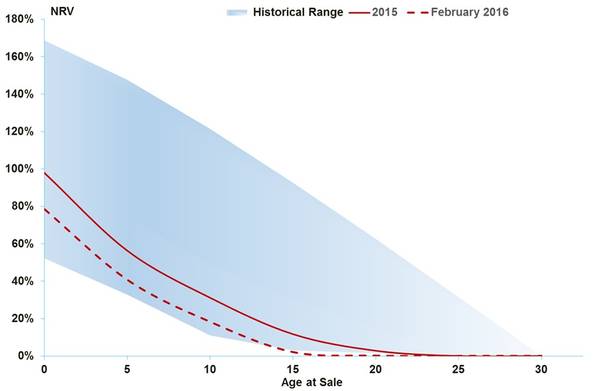

With earnings currently at OPEX or below, even 15-year-old vessels are now being valued at their realizable scrap value, plus a nominal mark-up for vessel-specific condition. Age beyond 15 years is now purely a number and has little impact on value. The extreme levels to which prices for old vessels have collapsed can be seen in Figure 1, which compares the current secondhand Panamax vessel values in terms of Net Replacement Value (NRV) with historical ranges.

Thoughts are no longer fixated on how low earnings and prices will fall; the general consensus is that both are at or near the floor. The focus is now on the shape of the downturn, or rather how long it will last. First and foremost, is there any hope for bulker earnings and prices in 2016?

In terms of downward momentum, the good news is that the end is nigh with an expectation that second-hand prices will bottom out at levels marginally below current values during 2Q 2016 for almost all ages and sizes of dry bulk carriers, MSI said.

This is underpinned by expectations of a minor rate correction in Q2, driven by a seasonal uptick in iron ore imports by China and strong South American grains exports. Enthusiasm should be tempered for the remainder of this year, however; the outlook for dry bulk supply/demand fundamentals in aggregate for 2016 is far from promising, with supply growth set to more than offset demand growth by a small margin.

Changing Demand Dynamics

According to MSI, the story is not much brighter for beyond this year – it is not until 2018 before we see any sustained improvement in market balances. Moreover, there are significant risks on the downside to this view.

MSI’s latest dry bulk report presents a scenario in which plausible downside risks to MSI’s forecast for Chinese and Indian coal imports and Chinese iron ore imports are realized, including a robust supply-side response. Under this scenario, MSI said it would not anticipate an uptick in market balances or time charter rates before 2020.