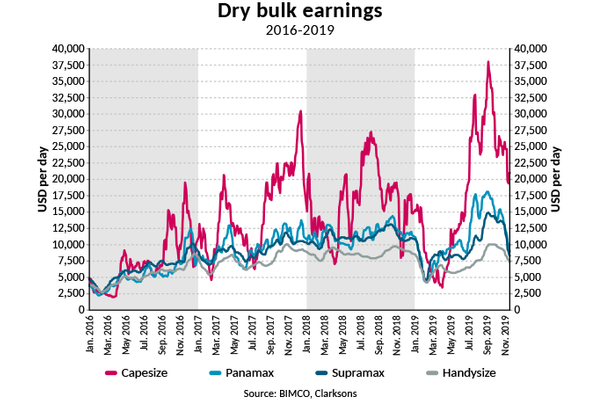

Freight rates down from multi-year highs as the market fundamentals make themselves felt.

The fundamental balance in the market has worsened in 2019 with supply growth outstripping demand, and BIMCO expects that this will continue into 2020.

Demand drivers and freight rates

After peaking in September, the fundamentals of the market have begun to drag on freight rates – although the rates remain above the average experienced so far this year, buoyed by a handful of positive developments during Q3.

For only the third time this year, monthly Brazilian iron ore exports exceeded 30m tonnes, with 31.2m tonnes exported in October. In 2018, this export level was reached in nine of the 12 months. Indications from Vale suggest that exports may face renewed pressure through to the end of the year, Although after falling to zero at the start of November, the number of spot cargoes being reported has increased.

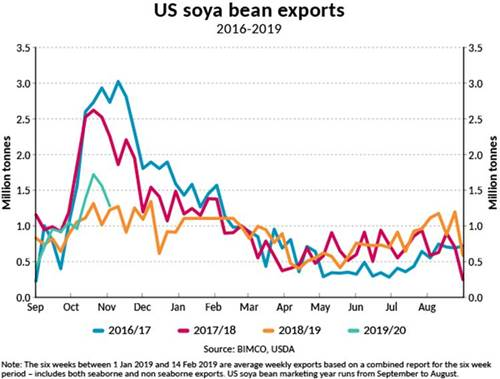

Despite rumored breakthroughs in trade talks, BIMCO expects that exports in the main US soya bean season will continue to be lower than those in previous seasons unaffected by the trade war. This is not only because of these tensions, but also due to the massive culling of pigs in China in response to the African swine flu. This has led to 41% fewer pigs in China than at the same time last year, dramatically cutting the country’s demand for soya beans. Furthermore, Chinese buyers have continued purchasing Brazilian soya beans, which is unusual, at a time when they would usually be importing from the US.

Fleet news

Dry bulk fleet growth in 2019 is already higher than it has been in any year since 2014. It is currently standing at 3.5%, and BIMCO expects it to rise to 4.1% by the end of the year. This is based on the expectation that a further 6m deadweight tonnage (DWT) will be delivered between mid-November and the end of the year, adding to the 36m DWT already delivered, and 0.9m will be demolished. This would bump the total demolition up to 7 million DWT.

Outlook

While earnings have remained at healthy levels moving into Q4, this has little to do with the market fundamentals. Instead, it is a continuation from the high freight rates seen in Q3, where a positive demand shock saved them from the doldrums they had experienced in the first half of the year.

The swing factor remains Chinese coal imports, which have grown by 9.6% in the first 10 months of the year. While this growth is expected to continue into the last two months of the year, policy decisions in China could have a large impact. Imports were curbed at the end of last year, as a result of domestic policies aimed at reducing emissions. This meant Chinese coal imports fell from June through to December, with imports in December 2018 dropping to less than half of those in the same month in 2017.

The fundamental balance in the market has worsened in 2019 with supply growth outpacing that of demand. BIMCO expects that this will continue into 2020 and the fleet to grow by around 3%. This will do nothing to help shipowners pass on the additional costs of the looming IMO 2020 sulphur cap, which is set to add even more pressure to already struggling bottom lines.

It remains unclear whether the high freight rates in Q3 were due to delayed cargoes from Q1 appearing on the market, or the pushing forward of Q4 cargoes. BIMCO expects the former, but fears that if the latter is to blame, then freight rates will continue to fall in the last quarter.