"The Iran war and the resulting disruptions to ship transits through the Strait of Hormuz have increased uncertainty for both the global economy and the dry bulk market. Around 4% of dry bulk cargoes and tonne mile demand typically sail through the strait and at present, and around 210 ships, equivalent to roughly 1% of the dry bulk fleet, are currently trapped in the Persian Gulf,” says Filipe Gouveia, Shipping Analysis Manager at BIMCO.

Given the high uncertainty over when transits may resume, we present two forecast scenarios. The “SoH closed” scenario assumes the strait remains effectively closed indefinitely, while the “SoH open” scenario assumes an imminent reopening. The longer the closure persists, the closer the market outlook will align with the SoH closed scenario.

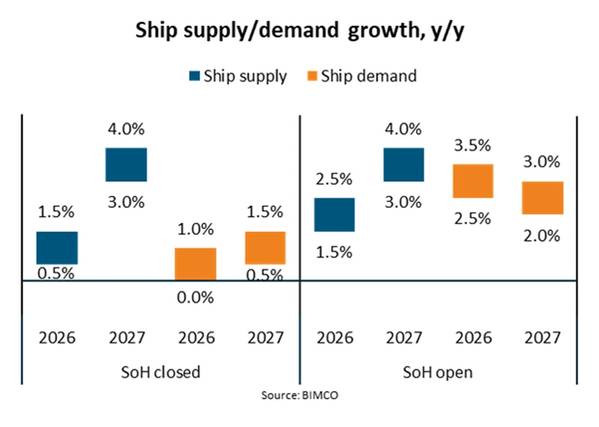

“If the strait remains effectively closed, the supply/demand balance is expected to weaken slightly in 2026, albeit from a high baseline, and to weaken significantly in 2027. If transits resume soon, we forecast market conditions to remain strong during this and next year, as the supply/demand balance strengthens in 2026 and slightly weakens in 2027,” says Gouveia.

Supply growth is expected to be broadly similar under both scenarios. Under the SoH closed scenario, fleet supply is forecast to grow by 0.5-1.5% in 2026 and by 3-4% in 2027. Under the SoH open scenario, supply growth is only around 1 pp higher in 2026. High deliveries in the panamax and supramax segments are driving fleet growth, while ship recycling is expected to remain low.

Differences between the scenarios are more pronounced on the demand side. Under the SoH closed scenario, demand is expected to grow by up to 1% in 2026 and by 0.5-1.5% in 2027. If the strait reopens, demand growth is forecast to be around 2.5 pp higher in 2026 and 1.5 pp higher in 2027, driven by stronger minor bulk and grain volumes. Around 9% and 6% of minor bulk and grain cargo volumes typically transit the strait.

The full return of dry bulk shipping to the Red Sea has been delayed by the Iran war, given an increase in the perceived risk of transiting the area. If safety conditions improve and ships return fully to the area, rerouting via the Cape of Good Hope would end, reducing average sailing distances and lowering tonne mile demand by 2%.

“The expected arrival of El Niño adds another uncertainty to the dry bulk demand outlook. Weather impacts associated with this phenomenon are not guaranteed, but they could disrupt Panama Canal transits, raise coal demand and affect grain harvests unevenly across regions,” says Gouveia.