As of end-June 2021, more than 100 turbine and foundation installation and maintenance vessels will be required for offshore wind projects planned over this decade.

More than 100 turbine and foundation installation and maintenance vessels will be required for offshore wind projects planned over this decade.

Almost all of the current fleet of international wind turbine installation vessels will be technically redundant as installation vessels by 2025 as a consequence of the rapidly growing wind turbine sizes, greater water depths and increase in foundation size. Demand will be satisfied by over 60 newly constructed or upgraded vessels -- presenting a $14 billion-dollar opportunity for engineering firms, shipbuilders and conversion yards, equipment suppliers, service providers and those who finance marine assets.

Foundation installation requirements are also rapidly changing. Market requirements are now shifting to purpose-built wind foundation installation vessels capable of handling the largest monopile foundations. More specialized vessels will be required for this purpose.

As well as uncertainties posed by the rapidly evolving technological terrain, installation vessel owners are also having to navigate their way through evolving local content requirements in Taiwan, Japan, the United States and elsewhere.

China is a relatively closed and busy offshore wind market with its own demand drivers. Chinese WTIVs are unlikely to operate outside of China. In fact, it is more likely to see smaller installation vessels redeployed to the Chinese market, especially as they become less technically suited to international demand.

These are the findings in a new report “International Wind Turbine and Foundation Installation Vessel Market” just completed by World Energy Reports.

The 70+ report provides a guide to understanding the drivers that will shape requirements in this growing, globalizing and technically evolving industry. The report examines the structure of the installation industry, profiles the underlying market drivers, forecasts wind installation activity through 2030 and identifies installation vessel technical requirements to meet future demand.

Introducing offshore wind turbine and foundation installation vessels

Until now installation requirements have been largely satisfied by WTIVs and heavy lift vessels deigned for the oil & gas and port/salvage market. Market requirements are now shifting to larger capacity WTIVs and purpose-built wind foundation installation vessels capable of handling the largest monopile foundations.

A WTIV is a self-propelled self-elevating jack-up with a crane capacity of 600 tonnes or greater for lifting a WTG set in 5-6 lifts. WTIVs perform a range of functions as part of the offshore wind farm supply chain.

A new generation foundation installation vessel is a self-propelled DP2/3 vessel with a large deck space for carrying foundations from the manufacturer's facility direct to site and with a crane capacity of 3,000 tonnes or greater.

Offshore wind overview

From the first eleven 450kW WIND TURBINES 5MW Vindeby Windfarm, commissioned in 1991 in Denmark, offshore wind has grown to reach over 32GW of cumulative installed capacity by the end of 2020 provided by 18 countries. Almost all capacity is bottom-fixed -- except for some floating wind pilot arrays.

Northwest Europe and China accounted for 99% of installed capacity at the end of 2020.

The UK was the single biggest market, accounting for 32% of global capacity by at the end of 2020. Germany was the second largest market with 24% of capacity. This activity has supported the development of a significant industrial base for wind farm component manufacture installation capabilities. Europe and the UK has taken three decades to industrialize the offshore wind supply chain. The 1990s and early 2000s where characterized by comparatively small demonstration projects aimed at testing offshore wind technology. Commercial scale wind farms only started to appear at the start of the last decade. Wind farm development in emerging non-European markets (Taiwan, Japan, the US) has been supported by European manufacturing capacity and installation vessels.

China has witnessed a surge in offshore wind activity since 2015, grid connecting 22GW of capacity by the end of 2020. The foundation of the current offshore wind boom is subsidies available for projects approved before the end of 2018 and grid connected by end 2021. Much of China’s initial wind farm activity can be classed as intertidal, in very shallow water falling within 10km offshore. More recently wind farms have moved outside of the tidal zone into offshore waters. China is a relatively closed and busy offshore wind market with its own demand drivers.

For a wind turbine and foundation installation perspective, we see three relatively distinct markets driving demand:

• International: This segment is considered largely open for all international assets. Over time, certain markets like Taiwan, Japan, the US, and South Korea will see an increased supply of locally flagged and owned assets at which time these markets will become increasingly locally content driven. Bottom-fixed solutions (up to 60-70m) will drive growth. Floating wind segment will develop through this decade in most of these markets, both for deeper water (over 60m water depth) or in shallow water poor soil conditions -- possibly for the Baltics and Taiwan.

• China: A discrete installation market, that may take assets from the international supply but is unlikely to contribute to the international supply side in the foreseeable future. Initially an intertidal market, China is developing as a bottom-fixed market.

• Vietnam: a largely intertidal market not requiring modern purpose built WTIVs/WTVFs.

In the mid- to long-term, we are tracking offshore wind projects in 38 countries. Our Base Case forecast identifies around 235GW of installed capacity by 2030, around 96% of which will be bottom fixed. This activity will drive the installation of over 9,300 wind turbines and foundation in the international market through 2030 and over 8,000 in China.

The international and Chinese market will be installing different turbines and foundations. The international market will be mainly supplied by three leading OEMs -- Siemens Gamesa Renewable Energy, GE and Vestas. The largest wind turbine installed today is the 8-10MW turbines. 12-14MW turbines will dominate mid-decade activity and 15MW+ turbines will be deployed at scale from 2027. The Chinese market will move away from 4-6.5MW turbines to 10MW and over by the middle of the decade. Summary of Market Size, Local Content Preference and Development Type. Source: WER

Summary of Market Size, Local Content Preference and Development Type. Source: WER

The speed of wind turbines output evolution has been rapid – larger wind turbines deliver higher outputs and higher capacity factors which leads to project cost reductions.

The chart below shows the evolution of international wind turbine sizes from 2010. The size of wind turbines at their tip is shown to scale with the Eiffel Tower and a next generation WTIV, similar to Jan de Nul’s Voltaire new building. The tip heights for the 12-14MW wind turbines deployed from 2022 will reach 250-260 meters. The next generation WTGs are expected to have 20MW output. Tip heights above 280 meters are expected.

Larger wind turbines output results in heavier and larger components (nacelle and hub, blades, and towers). The heavier components drive heavier foundations to support the increased wind turbines loads. The longer cardon fiber blades that all larger rotor diameter wind turbines have drive higher lifting heights.

Foundations will generally be installed in the year before turbine installation. The steel monopile has been the predominant bottom-fixed foundation solution in the international market to date. It is expected that the monopile will continue to be deployed in large numbers of international projects in the future. We anticipate that monopiles and jackets will account for over 95% of bottom fixed foundations through 2030. Larger wind turbines and deeper waters are resulting in very large monopiles, most of which cannot be installed by today’s WTIV fleet.

Wind farm construction and maintenance vessel fleet

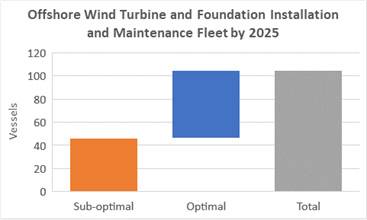

We forecast a global fleet of around 105 wind farm construction and maintenance vessels by 2025. Close to 60 WTIVs and foundation installation vessels will provide the backbone of the wind farm turbine and foundation installation capabilities by the middle of the decade. Although being suitable to perform wind farm maintenance duties, our forecast indicates that the majority will focus primarily on construction work.

An additional 45+ vessel, grouped as sub-optimal for installation activities, will support some construction work, particularly in China, as well as servicing important O&M demand.

The figures exclude some 125 oil & gas and port/salvage heavy lift vessels, some of which have been used to support offshore wind projects in the past and will occasionally provide solutions on specific project challenges in the future.

A $14 billion capex opportunity

WER's forecast identifies a demand of more than 35 optimal WTIVs and foundation vessels are required to meet international turbine and foundation installation demand through 2030 amounting to over $10 billion of capex. The Chinese market demand will be met with around 25 additional WTIVs and foundation vessels for close to $4 billion of capex. Details off the forecast are provided in our report.

For more information about the International Wind Turbine & Foundation Installation Vessel Market Forecast, please visit www.worldenergyreports.com