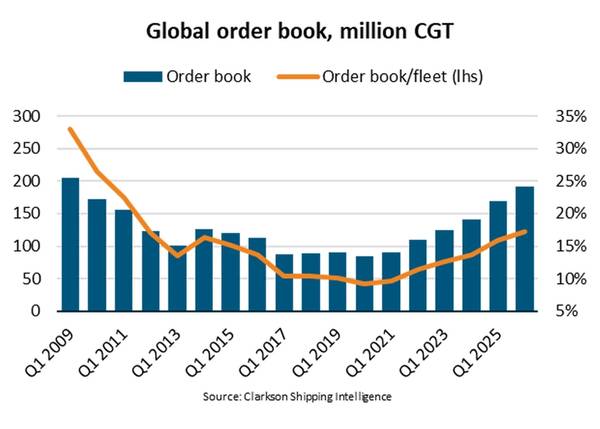

"By the end of the first quarter of 2026, the global shipping order book hit a 17-year high, reaching 191m Compensated Gross Tonnes (CGT). This is equivalent to 17% of the global fleet, the highest ratio since 2011. The order book has been boosted by higher newbuilding contracting throughout the 2020s and most recently by the highest quarterly crude tanker contracting in history,” says Filipe Gouveia, Shipping Analysis Manager at BIMCO.

During the first quarter of 2026, newbuilding contracting has risen 40% y/y to 17.6m Compensated Gross Tonnes (CGT), driven by a tripling of new tanker orders and a rebound in LNG tanker contracting. Overall, tankers have accounted for 32% of total contracting, the highest share since the second quarter of 2017. Despite this significant yearly increase, newbuilding contracting has decreased 17% q/q, amid an easing in dry bulk orders. Bulker contracting spiked during the last quarter of 2025, largely due to increased orders for capesize vessels.

“So far during the 2020s, newbuilding contracting has been 47% higher than the average during the 2010s, driven by stronger market conditions in the larger sectors, an overall larger fleet and an increased need for fleet renewal. This has contributed to an increase in newbuilding prices and longer lead times at shipyards, with 57% of contracting so far this year expected to be delivered after 2028,” says Gouveia.

Some shipping sectors now have relatively large order books. The order book to fleet ratio has risen to 22% for crude tankers, 19% for product tankers, 37% for containers and 40% for LNG. For crude and product tankers, these newbuildings are expected to support fleet renewal as 21% and 17% of the respective fleets are now over 20 years old, the age at which recycling is typically considered. By contrast, only 4% of the container fleet and 8% of the LNG fleet are over 25 years old, although these segments are expected to see higher demand growth.

Chinese shipyards remained the dominant choice for shipowners, accounting for 70% of contracting in the first quarter of 2026. Korean yards captured a further 20%, supported by stronger LNG tanker ordering. In contrast, contracting at Japanese yards fell 83% y/y to just 1% of new orders, the lowest share since at least 1996, reflecting limited capacity, long lead times and reduced competitiveness.

“In the medium term, the already swelling order books across several large shipping sectors could contribute to a slowdown in newbuilding contracting. Long lead times at shipyards and high newbuilding prices, combined with high market uncertainty concerning the Red Sea and the Strait of Hormuz sailings and alternative fuel availability, could also negatively affect contracting,” says Gouveia.